Get paid to pursue your hobbies

Get paid to pursue your hobbies

The shrewd layman's guide to tax deductions

This post is written for the minority of Americans who pay federal income tax (most do not), have at least one hobby and are willing to exchange one afternoon of their time for thousands of tax savings.

Motivating examples

Let’s start off with some examples.

Helen is a lawyer living in Boston earning $90,000 at a big firm (she has not made partner yet). However she really enjoys video games and has thought about streaming on Twitch and YouTube. Helen wants a new gaming computer with an NVIDIA GeForce 3090 (separate from her personal computer) and a full streaming setup, totaling about $8k. Helen can choose between

A) $5k cash to save or invest

B) $8k worth of equipment to use now

Steve is an unemployed yoga teacher in 2020 who received $40,000 in the form of enhanced COVID benefits. Steve likes introducing people to yoga and wants to convert a spare bedroom to a yoga studio for 1-on-1 yoga sessions. Steve can choose between

A) $2k cash to save or invest

B) $3k to pimp out his yoga studio

Rudolph is a full-time stay-at-home dad living in LA whose wife earns $300,000 as a general surgeon. Rudolph has a passion for fitness and has thought about starting a small personal training business. He wants to convert his garage into a gym for clients. Rudolph can choose between

A) Just under $5k cash to save or invest

B) $10k to convert his garage into a full-blown Crossfit-style gym

In theory Helen must use her new rig for streaming only. Personal gaming must occur on her Xbox one. Steve must use his old yoga mat when practicing for himself only. He must also restrict the usage of his expensive incense and nice speakers to his client sessions. And Rudolph must perform his personal workouts in his old gym. However, Helen is a prolific streamer and streams up to four hours a day and both Steve and Rudolph rehearse their 1-on-1 sessions in their studios without clients present. They may also offer zoom sessions.

Wait—how is this possible?

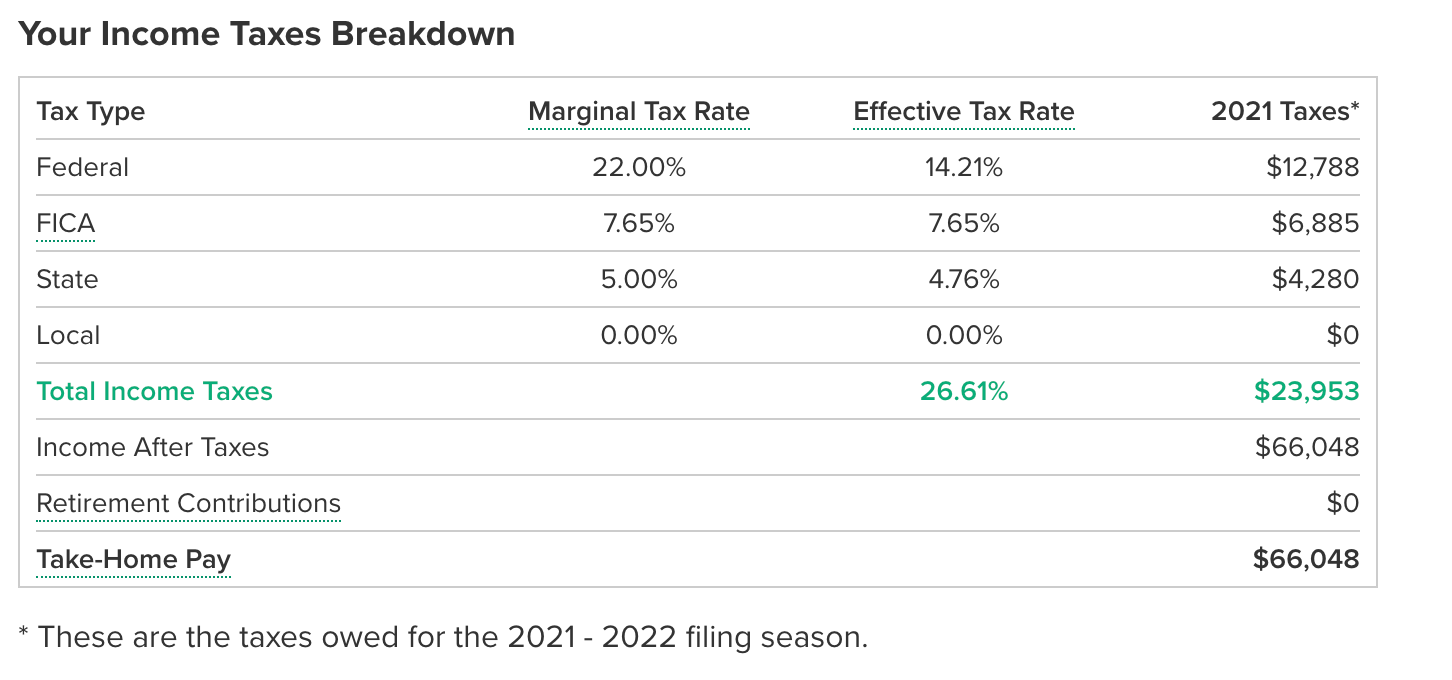

We start with Helen. In a normal year Helen earns $90,000 in Massachusetts. $90,000 is her taxable income.

Her marginal tax rate is 34.65% (22% federal 7.65% FICA and 5% state). In other words, Helen lost $0.3465 to tax on her 90,000th dollar (in contrast she lost only $0.0765 on her first dollar).

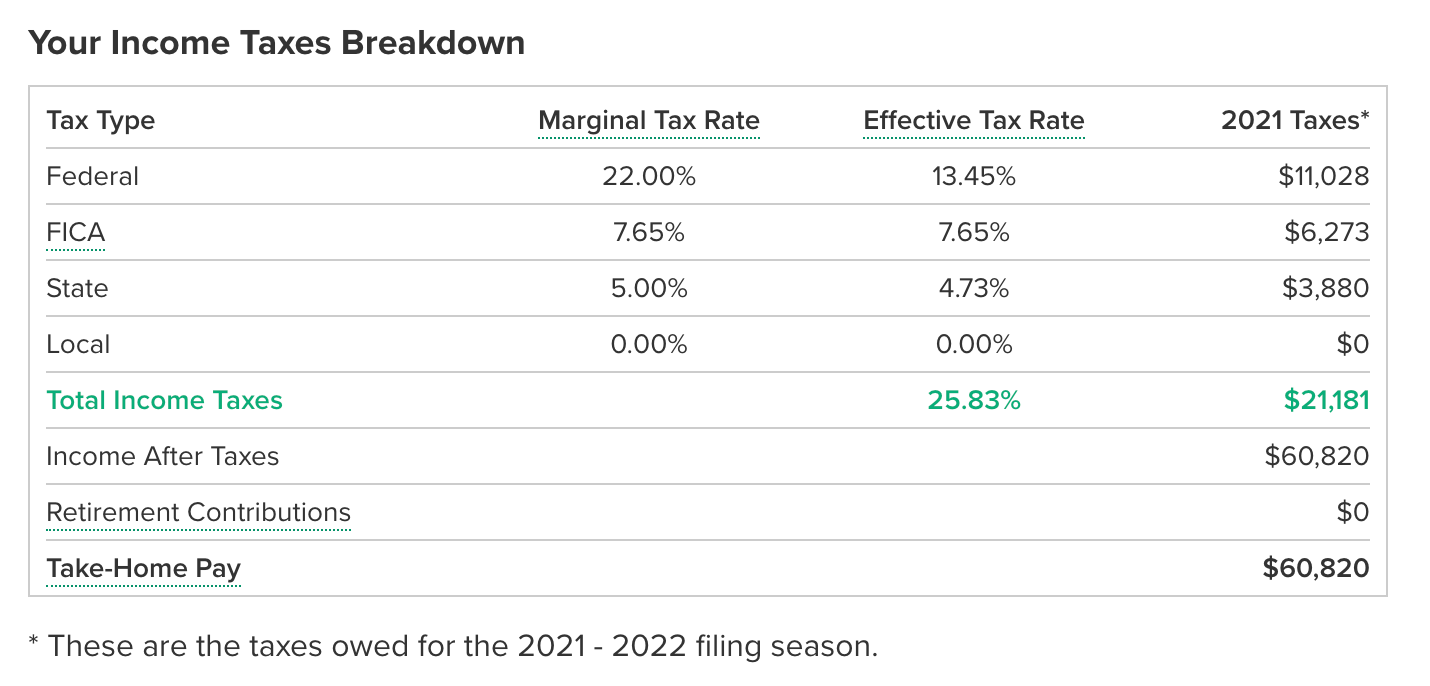

Let’s now say Helen needs about $8k for a good gaming rig which includes a top-of-the-line Alienware, a microphone, good lighting and a sturdy ergonomic gaming chair. If Helen deducts these from her $90,000 day job income on her Schedule C her taxable income will be reduced to $82,000. As we can see

Option A: ~$66k recovered from taxable income of $90k

Option B: ~$61k recovered from taxable income of $82k + $8k gaming rig

So we can see—if Helen chooses option A she takes home $66k. If she chooses option B she takes home $61k plus an $8k gaming rig. As always, the catch is that this rig must be used for her streaming projects and cannot be resold. If she happens to want the rig in this tax year, and she might buy it anyway (and not through her business), then she sort of gets to take home $69k worth of value.

If her goal is to maximize liquid cash and eventually paper wealth (equities, bonds, real estate—the usual investable universe) then of course she should take the $66k of cash. However, if she is content with $61k of cash (perhaps she has already maxed her 401(k)) then she can get “more” with option B.

I cannot stress this enough—she has to use her rig for streaming if she wants to claim this deduction (she does not, however, have to make money from streaming). If she turns around and sells it for cash somewhere then she is obviously breaking the law (though at her income level, the probability of audit is likely well below 1%).

The same logic applies to Steve and Rudolph.

A quick word before we move on. Yes, equipment (option B) depreciates while cash (option A) can be invested. However, even assuming strong investment gains (7% real) and an end to inflation—it would take Rudolph over ten years to reach the $10k required (after capital gains) to buy his home gym. That is also ten years of having no home gym for Rudolph. It would take Steve fewer years than Rudolph, but Steve is on a much tighter budget—Rudolph’s >50% marginal tax bracket logic does not apply to Steve.

The continuums

So should our three new friends pursue option A or B? I like to think about each possible deduction as a function of two variables.

Should I deduct? = F(auditability, utility)

A deduction scores high in auditability it is both “ordinary and necessary” for Helen’s streaming business and Steve’s and Rudolph’s studios. It scores low in auditability if it is not obviously useful to their newly founded businesses. Helen can absolutely deduct a new Xbox one if she uses it for streaming alongside her new gaming PC. But Rudolph can’t deduct an Xbox one for his studio, even if he uses it to show the occasional motivational Youtube video to his clients.

Auditability is not in your control. You can estimate auditability but at the end of the day the IRS decides whether a deduction passes an audit.

A deduction scores high in utility if you think it will bring you, and therefore your newly founded business, value. If you find personal fulfillment while working (as many do), and your new expense enhances this, your personal enjoyment will absolutely trickle down to your customers and clients and therefore enable continued success. It scores low in utility if you that is not the case. For example—I already have a maxed-out M1 Max MacBook Pro and considering I can only use one computer at a time, a Mac Studio wouldn’t necessarily score high in utility even though there are distributed workloads I could pass off to it as “ordinary and necessary” for my business.

Quick caveat: There is a third variable which is the probability of audit. We will discuss this in later posts.

Let’s visualize Helen’s situation on this two-variable continuum.

And mine

So as you can likely guess—the top-right is where you want to be.

Takeaway message

Rudolph is not going to squat more in his garage than at his gym. And Helen won’t play better on Overwatch when she’s streaming (actually, she might). Buying a new guitar is not going to make me better at guitar. It is better to not deduct at all than to be in the bottom quadrants.

But if you have hobbies you’re passionate about and you want to invest in them then our highly progressive tax system seriously incentivizes you to do so legally. Maybe that’s not such a bad thing. It’s probably better for the country anyway for you to put your skills out there. Maybe that’s by design. You decide what your hobbies are and it’s up to you to find value in and create value with them.

Disclaimers

I am neither a lawyer nor an accountant so please do not cite this piece in any official situation.

Lastly—make sure you don’t lose money on a business for more than three years in a row.

Appendix: How do I actually do this?

You could have an accountant do this for you (whose fee would wipe out your gains, unless you are rich), or you could

Open an LLC (this took me 10 minutes and cost $127 in NC)

Buy the stuff in your top-right quadrant

Download a .csv of all your expenses (my bank offers this and yours probably does too)

Make a new column called is_deduction and fill it with zeroes

For each each row, change is_deduction to 1 if it’s a deduction

Multiply the amount column with is_deduction and subtract this from your taxable income.

Voila, there is your new taxable income—finish up on TurboTax.

Starting a lawn mowing company on the side of my usual job. Plan on deducting all mowers and mowing attire I buy. I'm in the UK so the grass only grows for a few months of the year. Do I new to prorate my deductions to account for this?